One of the grand choices to make when you are a U.S. citizen, approaching a large bill or attempting to meet a debt obligation is: (Personal Loan vs Credit Card Loan)

- Should I borrow through personal loan (or a credit card) or

- Should I borrow through a credit card (or a credit-card type loan)?

It has no universal answer – it is a matter of how much you require, how quick you can pay, your credit history and how risk averse you are. We are going to step through the working of both of these, their advantages and disadvantages and situations when one is more likely to be considered than the other in this blog.

What We Mean by Loan personal and credit card loan

Before we get into the aspects of comparisons, it is important to get the roughly what each option entails.

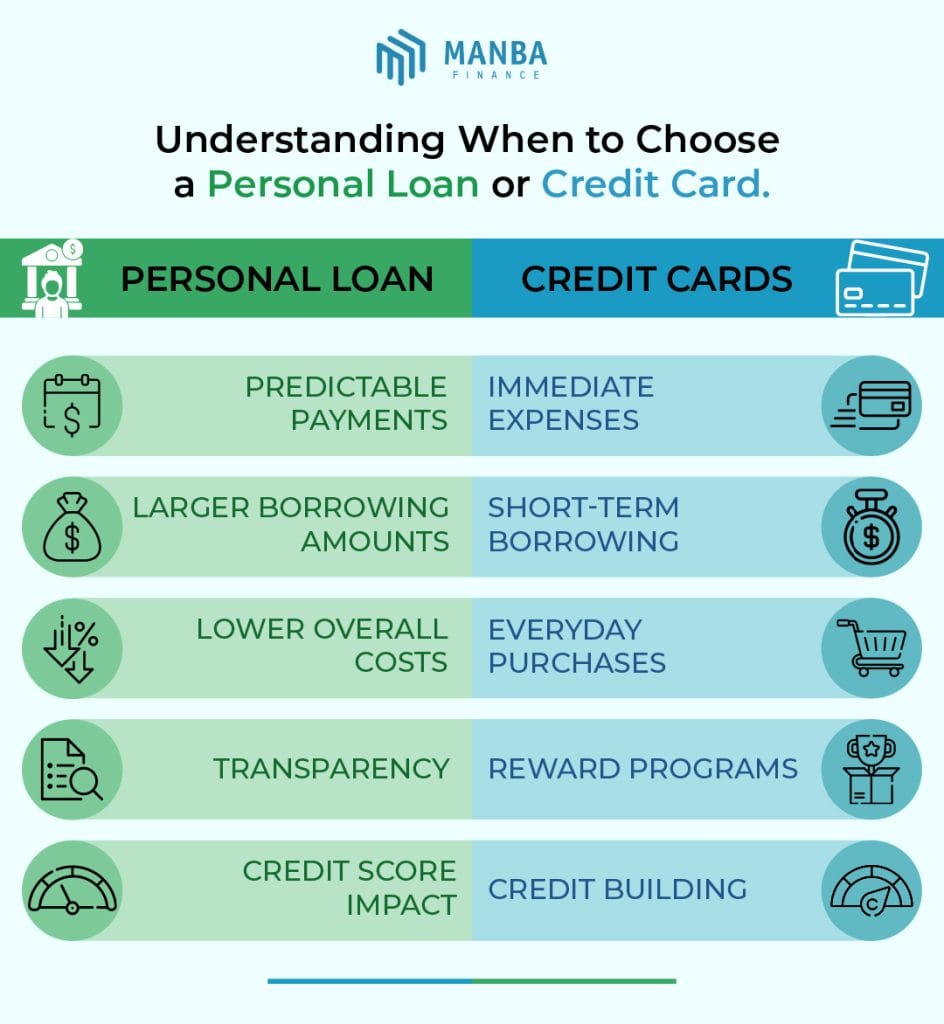

- Personal Loan: This is a lump sum of money that you borrow and pay the lender (bank, credit union, or online lender) in installments (usually in monthly installments) at a specific rate over a specific time (usually 1-7 years) period.

- Credit Card / Credit Card Loan: Under credit card, there is a revolving credit limit. There is a limit of how much you can borrow and repay, and then borrow, and so on. When you hold a balance between months, then you are charged interest.

When one speaks of a credit card loan, he or she may be talking about a charge on your card and actually having a balance (or transferring a balance) as opposed to a specialized lending product.

The main difference, is that personal loans are appropriate in large and one-time costs, whereas credit card works better with the everyday uses or regular costs.

Similarities Between Personal Loan vs Credit Card Loan

Despite the differences, these two options share important features:

| Feature | Personal Loan | Credit Card |

|---|---|---|

| Unsecured credit (often) | Yes — many are unsecured, meaning no collateral required | Yes — most cards are unsecured |

| Creditworthiness matters | Lenders look at credit score, income, debt-to-income ratio | Card issuers do the same when approving or determining rate |

| Fees & penalties possible | Origination fees, late fees | Annual fees, late fees, penalty APRs, balance transfer fees |

| Potential credit impact | Missed payments hurt credit scores | Same — late payments or high utilization hurt credit |

Both of them are unsecured (in most situations) and therefore your credit history and your income are very important in getting good terms.

Important Differences and What they Mean

1. Interest Rates & Variability

- Personal loans are usually provided with fixed interest rates throughout the life of the loan.

- It is almost certain that credit cards have variable APRs (which can increase or decrease depending on benchmark rates).

- This makes the credit cards more risky to the issuer (you may revolve or have a balance to another indefinitely) and thus the interest rates on the credit card are higher than personal loans (when the credit is comparable).

- Survey has reported that the U.S. personal loans have a range of about 6 to 36 percent, depending on their creditworthiness and other aspects.

- In the case of credit cards, when you fail to pay the balance after each month, you will very frequently see double-digit APRs. The risk is enhanced by the variable nature of the card and the rates of penalties.

2. Structure of Payments and predictability

- In case of a personal loan, you are aware of how much you will be paying per month over the term (except on the situation that you refinance or prepay).

- Using a credit card, you can pay at least based on your balance, APR, and policies; when you have a balance, you can pay dramatically differently each month.

- Due to it, personal loans are more predictable, which is beneficial in budgeting.

3. Access to Funds

- Personal loan provides all the funds at closing as a lump sum.

- Credit card provides you with a credit limit within which you can tap and draw as you wish.

4. Fees & Other Charges

- Personal loans can be charged with origination fees (percentage of the loan amount) or other set-up expenses.

- Annual cards, penalty charges, balance transfer charges, foreign exchange charges etc. may be charged on credit cards

5. Rewards / Benefits

- Personal loans are not usually based on rewards and cashback schemes.

- Credit cards usually do – thus you may get some advantages by being able to pay balances off in totality, through rewards, points, travel incentives etc.

6. Debt Consolidation and Balance Transfers

- A personal loan provides the opportunity to consolidate several debts with high rates of interest (such as credit card balances).

- Another type of credit-card-based consolidation is a balance transfer card (a credit card that offers low or no interest on transferred balances during a promotional period). According to reports, such cards typically have terms of promotion (15-21 months) and may be limited.

- What is better will depend on whether you can settle the debt before the promotion period expires and whether the amount you are getting in terms of consolidation does not exceed the transfer limit.

Current U.S. Rates How do they look?

As a rough idea of the price in the real world:

- In the case of users with a good credit score (690-719), users have recently been offered average rates of the mid-teens (around 14-17) on personal loans.

- Lower credit rates may skyrocket: in US people with a score below 630 are likely to consider APRs in the low-20s and sometimes higher, which can hit the limit of around 36 percent (the usual limit on consumer unsecured loans).

- In the meantime, the APRs on credit cards (on carried balances) tend to exceed the normal personal loans rates, and credit cards is costly when the balance remains unpaid.

Therefore, in case you are a good bet to get a good personal loan rate, you can do more to beat the interest charge of a credit card on anything you may be carrying than the statement period.

Also Read: Best Credit Cards in the U.S. to Build Credit

Strengths and Weaknesses: Who Wins (and When)?

Let us separate capabilities and shortcomings of each in more human terms:

✅When More Apposite than a Personal Loan

- You require a bigger lump-sum (such as the home improvement, car repair, medical bills, consolidation).

- You would prefer to be able to depend on the payments and detest to be surprised.

- You will have a long period to hold the debt.

- Your credit will score you a good APR.

- You are paying off the debt of higher interest and wish to pay it off as a single payment.

- Rewards are irrelevant to you, you are just aiming at cutting down costs.

⚠️Disadvantages / Cons of Personal Loans

- Monthly payment may be relatively high regarding a minimum on a credit card (particularly in the initial stages). Cautions has been taken that when it comes to making the loan payments, a credit card may seem less expensive on a monthly basis.

- You do not get the same money back (you can never borrow what you have paid back).

- Unless you have good credit you may have a high APR.

- Cost can be increased with origination and closing charges.

✅When a Credit Card / Revolving Credit Could Be better

- You should be flexible – you are not aware of the specific timing and values of costs.

- You are able to make the full payment on a monthly basis (therefore, no interest).

- You desire to enjoy rewards, points, cashback.

- You get a 0 percent APR deal or balance transfer offer and are able to pay off within that time.

- It is less and shorter-term – you do not plan to continue to have a debt weighing on you several months.

⚠️Credit Card Downsides / Risks

- Interest rates are high and erratic in the event that you have a balance.

- It is variable in nature and the cost may fluctuate without much prior notice.

- Unless you pay upfront, it may compound out of control, particularly with accrued interest.

- Large percentage use of credit is also bad on your credit rating (when your card balance is big in comparison to your limit).

- The promotional periods cease, rates increase.

Some Use-Case Scenarios

Let us give this in example situations you would encounter:

Scenario A: You require a loan of $10,000 in making repairs at home, repayment in 3 years.

- A personal loan may charge you 10-15% fixed, repurchased over a span of 36 months, paying a fixed amount of money monthly.

- It would be unsafe to use a credit card strategy unless there was a 0% APR deal and you were sure that you could complete it within the period.

- It is easy to see that your interest payments would easily exceed the cost of the personal loan when your APR on the card is 20 percent and you maintain the balance.

In this case, the personal loan is normally the safer one.

Scenario B: An emergency cost of 1000 dollars (e.g. medical or car repair)

- Suppose you have a credit card and wish to cover the $1,000 by the next statement, it might be okay to use the card (and receive some rewards).

- In case you are not able to pay it out completely, a short-term personal loan (or an offer of 0% on a credit card) may not be that expensive in terms of interest.

Scenario C: Incident involving several credit card debts

- Some card balances of 18%, 22%, 24%. In case you have obtained a personal loan at, say, 12-14% consolidation makes your life much easier and saves interests.

- Alternatively, a balance transfer card may come with 12-18 months with 0%APR. But you have to clear before the promotion is expired or you will be charged with an increase in the rate. The analysis of balance transfer options provided in survey would recommend that it is suitable when the debt is small and the promotional rate is large enough to get the debt repaid before the promotion rate runs out

The more desirable of the two, then, is strongly subject to the speed of payment and the extent of debt.

What to Ask Yourself (Checklist Before Deciding)

- How much do I need to borrow? In case of large amount personal loans will be more rational.

- How long will I carry the debt? In case of short-term (a few months), and you can pay in full, credit cards may be used. In case of longer, fixed-rate personal loan is safer.

- Am I a predictor or a flexible person? Fixed-pay personal loan is the better option in case you despise being caught off guard. Credit cards allow greater freedom (with increased risk) in case you want it.

- Am I eligible to have good offers on personal loans or credit cards? What will be offered becomes very dependent on your credit and income.

- Do I have enough discipline such that I will not get myself into revolving debt traps? Do you have the will power to pay off the balance monthly using a credit card? If not, the costs can spiral.

Better or Worse

o the majority of Americans, when a personal loan has a competitive interest rate and manageable monthly payments, it would tend to be the safer, predictable and in many cases cheaper path to medium to large or multi month borrowing. The credit cards are bright in case of smaller, temporary needs or when you can repay the balance in a short period of time (and, therefore, without paying the interests) or when you can take advantage of the promotion rate.

The best one is however based on your own circumstance- credit, income, period and discipline. Always calculate the numbers (monthly cost compared to total cost), make sure you read the fine print, and do not make assumptions.

Follow Us: Youtube